On August 15, the National Bureau of Statistics released economic data for July.

Economic indicators showed marginal weakening in July. Specifically, while export growth continued to rise, other metrics such as total retail sales of consumer goods, fixed-asset investment, industrial added value of major enterprises, and the national services production index all slowed compared to June. The fluctuations were mainly due to short-term factors such as extreme weather conditions and the timing of government subsidy disbursements.

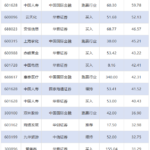

On the production side, industrial added value of major enterprises and the national services production index grew by 5.7% and 5.8% year-on-year, respectively. However, demand-side data was weaker, with July’s retail sales growing only 3.7% year-on-year—the lowest monthly rate this year.

With the allocation of the third batch of 69 billion yuan in government subsidies in late July, along with policies such as birth incentives, consumer loan interest subsidies, and business loan support for the services sector, the effects of policies aimed at boosting domestic demand, consumption, and public welfare are expected to strengthen. Some analysts suggest that macroeconomic policy support should be intensified in the second half of the year, including fiscal stimulus, further central bank rate cuts, and stronger measures to stabilize the real estate market.

Fluctuations in Some Economic Indicators

On the demand side, exports rebounded further in July, while consumption and investment slowed.

Despite a decline in exports to the U.S. due to tariff adjustments, China’s overall exports remained resilient, performing better than expected. In July, total goods trade reached 3.91 trillion yuan, up 6.7% year-on-year. Exports rose 8.0%, accelerating by 0.8 percentage points from June, while imports grew 4.8%, up 2.4 percentage points.

Exports remained strong in July, with Chinese firms actively diversifying into non-U.S. markets. Imports surged, partly due to eased U.S. export restrictions, particularly in high-tech products such as aircraft engines and integrated circuits.

Retail sales in July totaled 3.88 trillion yuan, up 3.7% year-on-year but slowing by 1.1 percentage points from June. Sales of home appliances, office supplies, furniture, and electronics maintained double-digit growth, supported by trade-in policies. Summer travel and leisure-related services also saw robust demand.

Retail sales growth slowed in July partly due to temporary pauses in trade-in subsidy programs in some regions. However, the recent allocation of 69 billion yuan in subsidies is expected to boost August sales.

From January to July, fixed-asset investment (excluding rural households) reached 28.82 trillion yuan, up 1.6% year-on-year but slowing by 1.2 percentage points from the first half. Manufacturing investment grew 6.2%, infrastructure investment rose 3.2%, while real estate development investment fell 12%, with the decline widening by 0.8 percentage points.

After adjusting for price factors, real fixed-asset investment growth was around 4%-5%, indicating steady expansion. The slowdown was attributed to extreme weather disruptions, external uncertainties, weaker returns on investment, and structural shifts as traditional sectors like real estate decline while emerging industries grow.

Emerging industries, though still small, are expanding rapidly. Investment in aerospace, computer equipment, and IT services grew by 33.9%, 16%, and 32.8%, respectively, from January to July. Renewable energy investments (solar, wind, nuclear, and hydro) surged 21.9%.

Policies to Boost Demand and Stabilize Real Estate Needed

China’s economy grew 5.3% in the first half of the year, outperforming expectations despite external uncertainties and laying a solid foundation for achieving the annual growth target of around 5%. While July data showed marginal softening, policy support is being ramped up.

A July 30 Politburo meeting emphasized maintaining policy continuity while enhancing flexibility to stabilize employment, businesses, markets, and expectations. Fiscal and monetary policies should be implemented effectively to stimulate domestic demand, boost consumption, and encourage private investment.

Despite fluctuations in some July indicators, cumulative growth remains stable, with employment and prices steady. The long-term fundamentals of China’s economy—resilience, advantages, and potential—remain intact. Policy support, market demand expansion, and industrial upgrades will sustain stable growth.

July’s economic performance was slightly weaker than June’s but remained broadly stable. High-tech industries, trade-in-related consumption, and equipment manufacturing investment maintained strong growth, continuing trends seen earlier this year.

Since June, some economic indicators have slowed due to extreme