The shift of international investment capital into the Vietnamese real estate market.

As global capital undergoes a major restructuring, Vietnam is strengthening its position as a stable market, attracting international investors moving from high-risk markets to economies with solid growth. Compared to other ASEAN countries, Vietnam stands out in three key factors: growth, stability, and development potential.

From “riding the wave” to “ecosystem”

“Vietnam is building a clear competitive advantage over economies like Thailand, Indonesia, or Malaysia,” said a director from the Institute for Informatics and Applied Economics Research. “If this trend continues, the development gap between Vietnam and other countries in the region could narrow faster than previous forecasts.”

The biggest difference between Vietnam and competitors like Malaysia is its stable political foundation and aggressive infrastructure investment. The Vietnamese government currently commits about 7% of GDP to infrastructure development—one of the highest rates in the region, creating a “safe corridor” for foreign capital inflows.

|

With an estimated market capitalization of about $1.5 trillion—three times GDP—the Vietnamese real estate market has become a “safe haven” and “effective profit channel” for international investors. Foreign capital flowing into Vietnam is no longer short-term speculative, as in the 2010-2012 cycle, but has shifted to direct investment in assets with stricter criteria.

According to a CEO from FIDT Investment Consulting and Asset Management Company, this capital can be classified into four main groups. The Northeast Asian group (Japan, South Korea) focuses on operational models, often “following the supply chain” of manufacturing and logistics. The Singapore group has a long-term vision, willing to “go big” into projects with transparent roadmaps. The “Alpha” strategic group seeks superior profits through joint ventures and asset restructuring. The opportunity fund group takes advantage of market correction phases to accumulate high-quality assets. For European and American investors, they are ready to participate in highly complex projects, including restructuring or developing assets with value-added potential.

Unlike the 2013-2014 period, when foreign capital focused on acquiring cheap assets, the current trend is long-term, selective investment tied to urban development. “Foreign capital today is not just looking for assets, but also for ecosystems to develop,” the CEO emphasized. Investors are not simply buying a building. They are participating in building megacities, smart industrial parks, and data centers.

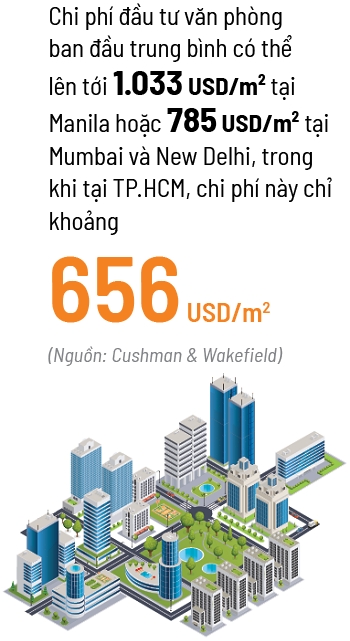

A director from the Leasing Department at Cushman & Wakefield Vietnam noted that Vietnam has a competitive advantage in attracting Global Capability Centers (GCCs). Vietnam also has a more competitive initial investment cost compared to India and the Philippines. According to a Cushman & Wakefield report, the average initial office investment cost can be up to $1,033/m² in Manila or $785/m² in Mumbai and New Delhi, while in Ho Chi Minh City, this cost is only about $656/m².

Foreign capital changes its taste

In the race to attract capital, ESG (Environmental, Social, and Governance) standards are no longer an “option” but have become a prerequisite for accessing international capital. Reports show that projects meeting ESG standards in Vietnam can see price increases 25-30% higher than surrounding areas.

|

“Over the past ten years, we have observed that the real estate selection standards of multinational corporations, especially high-tech FDI, have changed significantly. Previously, the first factors considered were usually location, infrastructure connectivity, and cost. Now, the evaluation weight has clearly shifted to project quality. Among these, green criteria and ESG requirements have almost become core measures to confirm the suitability of an industrial park or office building,” the director said.

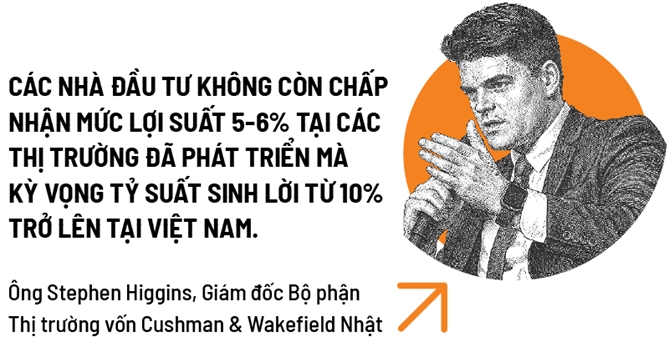

A director of Capital Markets at Cushman & Wakefield Japan noted that investors from developed economies are increasingly prioritizing sustainable projects to ensure long-term operational performance. They are no longer accepting yields of 5-6% in developed markets but expect returns of 10%