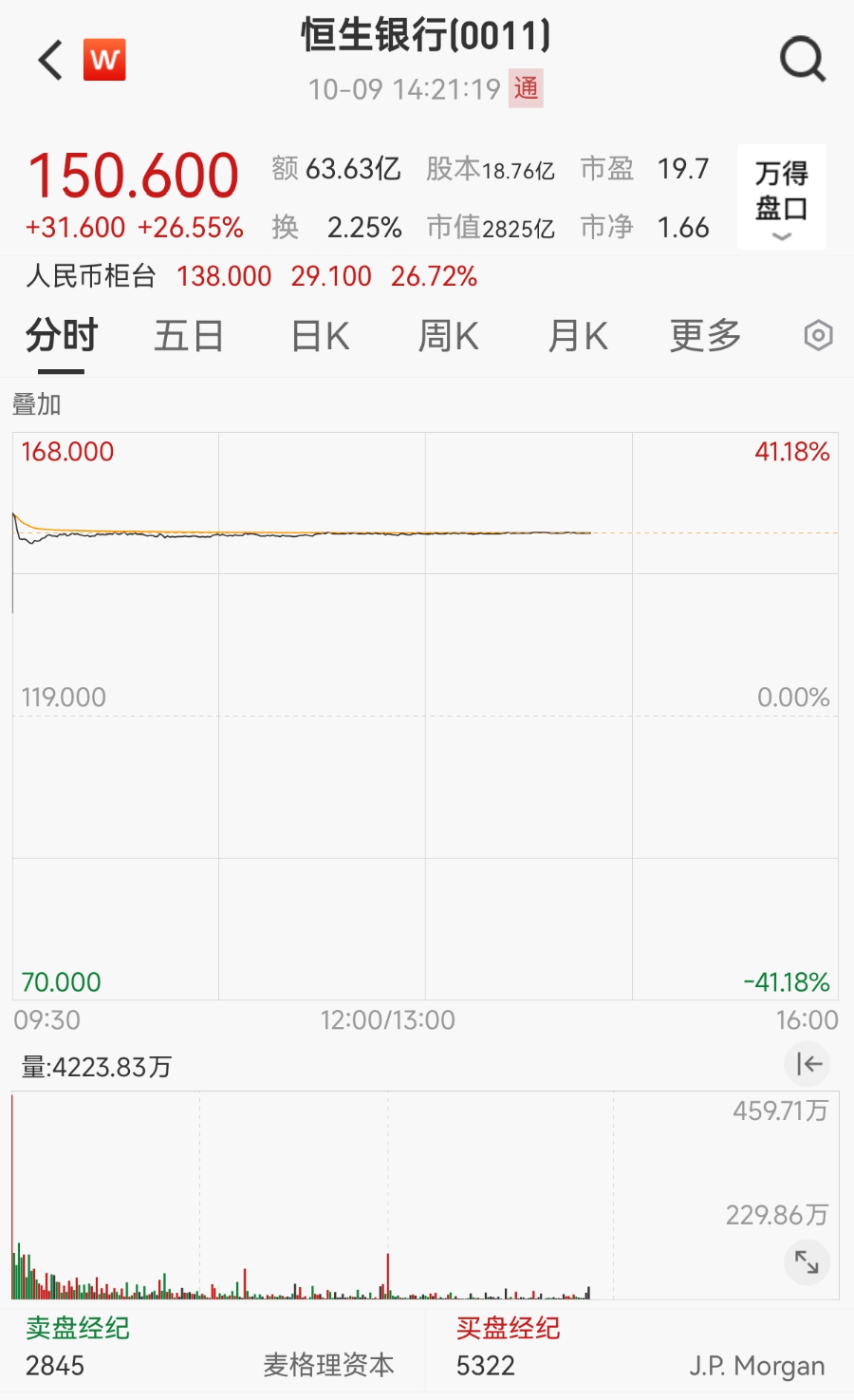

On October 9, Hang Seng Bank (0011.HK) shares surged up to 41% during trading, reaching HK$168 per share and hitting a record high. As of 14:20, the stock was up 26.55% at HK$150.60 per share. Notably, its controlling shareholder HSBC Holdings (0005.HK) fell 6.69% to HK$103.20 per share.

In terms of news, HSBC Asia Pacific plans to privatize Hang Seng Bank with a 30.3% premium. On October 9, HSBC Holdings and Hang Seng Bank jointly announced that HSBC Asia Pacific, as the offeror, has requested Hang Seng Bank’s board to propose to shareholders a scheme to privatize Hang Seng Bank through a scheme of arrangement. According to the proposal, Hang Seng Bank shares will be cancelled in exchange for a cash payment of HK$155 per share, valuing the transaction at approximately HK$290.3 billion. This consideration represents about a 30.3% premium over Hang Seng Bank’s previous closing price of HK$119.00 per share.

According to the plan, the privatization transaction must be completed or waived by September 30, 2026, or an earlier date. The announcement disclosed that Hang Seng Bank has established an independent board committee as required by the takeover code, which will advise on whether the proposal is fair and reasonable and how to vote.

Statistics show that since its listing on the Hong Kong Stock Exchange in 1972, Hang Seng Bank has been listed for 53 years, with its market capitalization growing from approximately HK$1.7 billion initially to over HK$280 billion currently, representing an increase of more than 160 times. If the privatization is completed, Hang Seng Bank will become a wholly-owned subsidiary of HSBC, ending its 53-year listing history.

Institutions: Short-term Pain but Long-term Benefits

If the proposal is approved, what impacts are expected on Hang Seng Bank? Analysis reveals that financially, according to the plan, Hang Seng Bank shareholders will still receive the third interim dividend for 2025, which will not be deducted from the scheme consideration. However, other dividends declared after the announcement but before the scheme becomes effective will be deducted from the scheme consideration. In terms of operations and management, the announcement states that Hang Seng Bank will retain its independently granted licensed bank recognition under the Hong Kong Banking Ordinance and maintain independent corporate governance and branch network.

Regarding the financial impact on HSBC Holdings, HSBC expects that by eliminating the earnings deduction from Hang Seng Bank’s non-controlling interests, the proposal will increase earnings per ordinary share. However, the transaction will still have some impact on HSBC Holdings’ capital adequacy ratio. To restore its CET1 ratio to the target operating range, HSBC Holdings stated it will achieve this through capital generation from its own operations and by not initiating any further share buybacks for three quarters starting from the announcement date.

J.P. Morgan’s latest report suggests that while this transaction brings short-term pain, it has positive long-term benefits for HSBC Holdings. Even without considering revenue synergies or cost optimization, due to the elimination of Hang Seng’s minority interest, J.P. Morgan estimates that HSBC’s 2027 earnings per share and dividends could be 1.5% and 3.1% higher than their baseline forecast.

Both Hang Seng Bank and HSBC Holdings Faced Profit Pressure in First Half

Notably, in the first half of 2025, both Hang Seng Bank and HSBC Holdings faced certain profit pressures. Specifically, interim results show that Hang Seng Bank’s total operating revenue before expected credit losses was HK$20.975 billion in the first half, a 3% year-on-year increase; profit attributable to shareholders was HK$6.88 billion, a 30.46% year-on-year decrease. HSBC Holdings’ revenue for the first half was HK$34.122 billion, an 8.50% year-on-year decrease; profit attributable to ordinary shareholders was HK$11.51 billion, a 30.60% year-on-year decrease.

Regarding the first-half performance, Hang Seng Bank’s Executive Director and Chief Executive Officer previously stated that market uncertainties persisted in the first half of 2025, with trade tariffs, continued high interest rates, and prolonged pressure on